What We’ve Learned About Fiscal Policy Since Keynes

Ninety years of economic research have refined (and, in important ways, qualified) Keynes’s boldest claims.

Ninety years after the publication of John Maynard Keynes’s The General Theory of Employment, Interest, and Money in February 1936, it remains one of the most influential economics books ever written. At the height of the Great Depression, Keynes gave policymakers a new framework: when aggregate demand collapses (as it did during the Great Depression), governments should incur debt, increase spending, and cut taxes to stabilize output. Budget deficits are not always a vice in this sense (as they had historically been viewed). In moments of crisis, fiscal policy can supposedly rescue capitalism from itself.

Few books have had more policy impact than The General Theory.

But ninety years of economic research have refined (and, in important ways, qualified) Keynes’s boldest claims. The modern empirical literature on fiscal multipliers actually looks very different from the simple textbook Keynesian model many students still encounter.

The multiplier is the central concept in Keynesian economics. It simply measures how much GDP increases when government spending rises by $1. In early Keynesian models, the answer was often $1.50, $2.00, or even more. Some have even argued that deficits could pay for themselves. With a marginal propensity to consume of 0.5 (that is, a consumer spends half their income), the textbook multiplier is 2. The logic is mechanical: one person’s spending becomes another’s income, which becomes more spending, and so on.

But the modern evidence suggests that reality is more restrained: people’s propensity to consume, as well as fiscal multipliers, are generally much lower than previously thought.

In more recent work Hoover Institution economist Valerie Ramey, she finds that for general government purchases (think tanks and defense spending), the bulk of credible multiplier estimates in advanced economies lie between 0.6 and 1.0.

In plain English: on average, a dollar of government spending tends to raise GDP by less than a dollar, or at best roughly one-for-one. But remember, deficit financing also adds debt, which will eventually need to be paid back in part through taxes that have their own fiscal multipliers, often higher in magnitude.

On the face of it, extremely high multipliers and fiscal self-financing may seem implausible. From the 2008 global financial crisis to the COVID-19 pandemic era, many countries have embarked on massive spending and stimulus programs, yet government debt continues to rise across countries.

These findings do not come from just one study. It emerges from a variety of places: structural vector autoregressions, narrative identification methods, calibrated New Keynesian models, and cross-country panel evidence. Once researchers standardized the computation of multipliers (using cumulative present-value methods rather than peak elasticities), estimates narrowed considerably.

Some of this might suggest that large crowding-out effects, stemming from higher interest rates induced by more debt, reduced private investment, or offsetting private behavior often dampen the textbook multiplier.

These facts don’t mean fiscal policy “doesn’t work” or shouldn’t be used during recessions altogether. Even if fiscal multipliers are close to zero, there is a case to be made that governments should play a role in providing additional social insurance during recessions and help to smooth consumption, particularly among the poor.

Are fiscal multipliers larger in recessions? Keynes’s General Theory was born of the Great Depression (published in 1936), and modern defenders of aggressive stimulus often argue that multipliers are especially large in bad times. Yet the evidence here is more cautious than the rhetoric suggests. Ramey’s work finds that while some nonlinear models find large recession multipliers, these results are fragile: more robust estimates still show multipliers around one or below, even in downturns.

There is somewhat stronger evidence that multipliers can be larger when monetary policy is constrained, such as at the zero lower bound on interest rates. In those special circumstances, some fiscal multiplier estimates rise above one. However, those are rare contingent cases and not the general rule. It is also true that lower income individuals with little in savings will spend more of their stimulus checks. But one also can’t forget the possibility that such fiscal transfers, if excessive, can contribute to inflation, as seen in the early 2020s.

Tax policy presents a different picture regarding fiscal multipliers. Narrative studies (particularly those pioneered by Christina and David Romer) of exogenous tax changes often find large tax multipliers, with absolute values between –2 and –3. That is, a permanent $1 tax cut can raise GDP by more than $2. Yet here again, theory and calibrated New Keynesian models often imply much smaller effects.

But if it is truly the case that tax multipliers are larger than government spending multipliers, as others, including the authors of Austerity: When It Works and When It Doesn’t (Alberto Alesina, Carlo Favero, and Francesco Giavazzi) find in their own research, then it’s possible to actually create GDP growth if government spending is reduced by the same amount that taxes are cut. Hence, running a balanced budget in a so-called austerity plan to cut government spending when accompanied by tax cuts could be much less austere (this was something these authors suggested to Europe near the peak of the European sovereign debt crisis in the 2010s).

The tension between narrative evidence and structural models remains unresolved. But the key point is this: fiscal policy is not a single blunt instrument. Spending, taxes, transfers, expectations, financing methods, and monetary responses all matter.

Perhaps the most important lesson of the last 15 years is methodological. The profession had largely neglected fiscal policy research from the 1970s through the early 2000s. The global financial crisis (which spurred renewed drives for fiscal policy as stabilization policy in legislation such as the American Recovery and Reinvestment Act) forced a renaissance including recognition that fiscal changes are often anticipated (“fiscal foresight”), which alters measured effects, improved identification strategies using narrative records and natural experiments, better methods for computing cumulative multipliers rather than misleading peak elasticities, and greater attention to state dependence and institutional context.

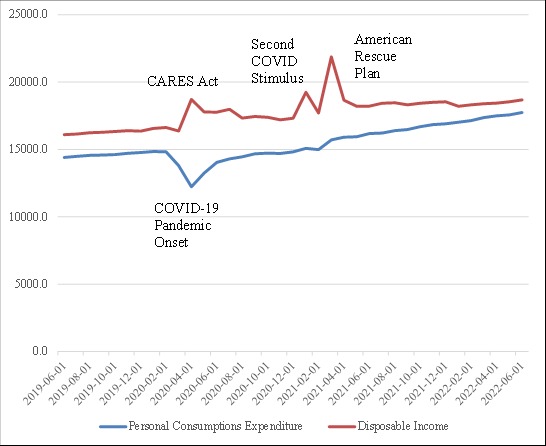

Analyzing tax rebates shows even more direct evidence. When tax rebates were paid out in 2008 and 2020, consumer spending merely budged, implying that fiscal stimulus checks are largely saved, rather than spent, contrary to the advocacy of uber-Keynesians.

The 2008 Tax Rebate and Consumer Spending

Early 2020s Stimulus and Consumer Spending

In that sense, Keynes was directionally right; demand shortfalls (like those seen during the Great Depression) matter, but his followers have quantitatively overstated multipliers in many environments. Keynes wrote in a different time, a world of fixed exchange rates, gold constraints, and limited automatic stabilizers. Today’s economies operate with floating exchange rates, independent central banks with Taylor-rule reaction functions (that is central banks increase rates in response to inflation and lower rates in response to significant unemployment), and massive transfer payments systems. Much of the stabilization function Keynes envisioned is now embedded in automatic stabilizers: unemployment insurance, progressive taxation, and transfer programs that expand without discretionary legislation. These did not exist in large part prior to the Great Depression.

In modern advanced economies, the first line of defense against recession is monetary policy. The second is the built-in fiscal architecture. Discretionary stimulus in the form of large, sudden spending programs may still have a role. But the case for expecting multipliers of two or three in ordinary circumstances is not supported by the weight of current evidence.

Ninety years on, Keynes remains an important read to consider. He forced economists to confront the possibility that market economies can settle into prolonged slumps. He legitimized countercyclical policy and reshaped the relationship between economics and the state.

Keynes’ work was centered on reviving the world from the Great Depression, something most nations have not seen since. Keynes also argued that nations should run fiscal surpluses in good economic times while running fiscal deficits in bad times.

The modern empirical literature (carefully summarized by scholars like Valerie Ramey) suggests a more nuanced view: fiscal policy can stabilize output, but its effects are typically moderate, context-dependent, and often offset by private-sector responses.

The General Theory at 90 reminds us in general that economic ideas must be tested, quantified, and revised. Keynes taught economists to think in terms of aggregate demand. The last three decades have taught us to measure it more carefully.

In an era of renewed debates over deficits, industrial policy, and fiscal expansion, that empirical discipline may be Keynes’s most important legacy of all.

Jonathan Hartley is research fellow at the Civitas Institute, a Policy Fellow at the Hoover Institution, and senior fellow at the Foundation for Research on Equal Opportunity.

On Keynes, Coase, and Posner

The differences between Keynes, a pioneer of government spending and intervention, and Ronald Coase, a pioneer of maximizing growth by minimizing transaction costs, are as far as can be.

What We’ve Learned About Fiscal Policy Since Keynes

Modern evidence suggests that reality is more restrained than Keynes thought: people’s propensity to consume, as well as fiscal multipliers, are generally much lower than previously thought.

Keynes’s 'General Theory' as an Emergency Brief

The 'General Theory' was born from a specific historical emergency: the failure of postwar governments to deal with a depression rooted in the unimaginable destruction of wealth and the corresponding monetary disequilibrium.

.jpg)

.png)

Get the Civitas Outlook daily digest, plus new research and events.

Get the Civitas Outlook daily digest, plus new research and events.